Malaysia – Looking to 2030: towards a high-income economy?

An open economy based on dual specialisation (in commodities and electronics), Malaysia has a dynamic growth outlook and robust macroeconomic fundamentals.

In the medium term, the aim is to become a high-income country by 2030: an achievable target but one that will mean avoiding the middle-income trap into which the country could fall if it fails to implement the fiscal and structural reforms needed to support growth.

Fiscal consolidation – begun following the Covid-19 crisis – is on track, aimed at redirecting revenue towards productive investment rather than subsidies.

However, certain risk factors, both external (impact of the closure of the Strait of Hormuz on value chains, trade dependence on China and the United States) and internal (political stability of the coalition and forthcoming elections), darken the horizon.

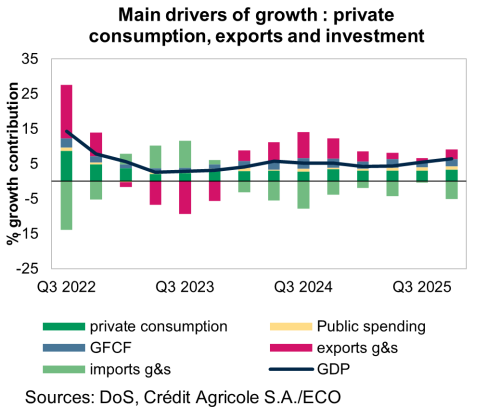

A strong end to 2025

Malaysia has returned to cruising speed following the recession triggered by the Covid crisis. After the economic upturn of 2022 (9% growth), GDP growth remained high (3.5% in 2023 and 5.1% in 2024), pointing to real resilience and a rapid recovery, despite poor management of the Covid crisis at the political level.

GDP growth in 2025 came in at 5.2%, ahead of the consensus. This was driven in particular by quickening growth in the last quarter, at 6.3%, driven by all components: strong exports, sustained investment (up 9.5% year on year) and private consumption (up 5.4% year on year), still supported by huge subsidy programmes (energy and food products).

The US import tariffs announced in April 2025 have had no major economic repercussions: private consumption, exports and the tourism sector have remained pillars of economic stability. The country also continues to benefit from a flood of foreign direct investment (FDI) into the semiconductors and data centres sector, driven in particular by positive momentum in artificial intelligence. The financial ecosystem does not appear to be under immediate threat of systemic risk and inflation remains under control.

Inflation is expected to pick up slightly in 2026 while remaining close to the central bank’s 2% target. The combined effects of higher oil prices, lower fuel subsidies and an across-the-board sales and services tax (SST) are likely to lead to a moderate increase in inflation, though the latter should remain below the 3% target. With the base rate at 2.75% (last cut in June 2025), the central bank still has some room for manoeuvre. The ringgit, which gained ground against the dollar in 2025, buoyed in particular by strong exports, has, like all emerging currencies, been overtaken by the conflict in the Middle East, though it has not fallen too far.

Aiming for high-income economy status

In the medium term, the goal is for Malaysia to become a high-income country and establish itself as one of the world’s top 30 economies by 2030. This planned economic expansion is part of the “Ekonomi Madani” model, which is underpinned by two key priorities: Raising the ceiling (becoming a flagship destination for investment, a leader in high-tech innovation and the global leader in Islamic finance) and raising the floor (reducing inequality, developing infrastructure and providing universal access to education and social welfare).

Raising the ceiling: riding the AI wave

Malaysia is one of the biggest beneficiaries of the recent boom in the digital economy and associated new industries (e.g. semiconductors).

The country continues to leverage the AI cycle to attract investment in data centres and the semiconductor sector. Inward foreign direct investment increased by 3.7% in 2025 to around $14 billion, driven by American, Singaporean and Hong Kong companies. Projects approved over the first nine months of 2025 totalled $67 billion (up 13.2% year on year). These investments are concentrated in services (66%) and manufacturing (33%). Malaysia enjoys an excellent business environment at the regional level, giving it a competitive edge over other countries in the region, encouraged by legislative measures such as tax exemptions on foreign sourced-dividend income.

The largest single export item is still electronic components and devices, totalling $151 billion in 2025, nearly 40% of total exports. The country thus benefits from its position as a platform in the value chain to attract investment. The objective, of course, is to move higher up the value chain, thus controlling a larger share of it and reducing reliance on inputs, with electronic components and devices also accounting for 32% of total imports.

Raising the floor: pursuing more inclusive development

Despite vigorous economic growth, the country still suffers from pronounced inequalities that hamper its development. Access to basic services such as health, education and employment remains particularly challenging for some rural communities, particularly in the eastern part of the country. Revenue from natural resources is not yet sufficiently channelled towards productive expenditure, social mobility remains very low and inequalities are high; the country’s Gini coefficient[1] is particularly high for the region, coming out at 40.7, compared with 34.9 for Indonesia, 33.5 for Thailand, 36.1 for Vietnam and 30.7 for Myanmar. However, there are plans to streamline subsidies and harness the resulting savings to invest in human capital.

The government has launched a series of infrastructure megaprojects to improve connectivity between regions. However, these projects often face hurdles in terms of funding or political acceptance. The planned high-speed rail line between Kuala Lumpur and Singapore – a flagship project aimed at strengthening cooperation between the two regions – is currently at a standstill, hampered by local political conflicts, high costs and a slow bidding process that puts Chinese and European companies in competition with one other.

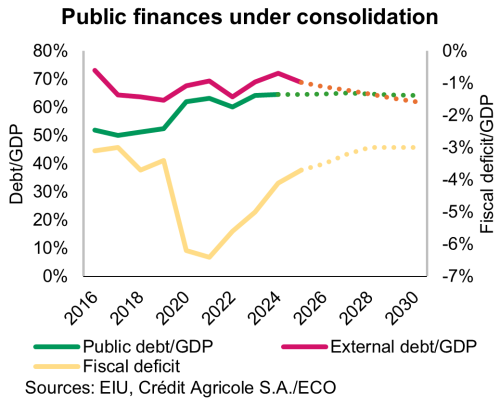

Fiscal consolidation: the government’s key priority

Imbalance in the public finances: a legacy of the Covid-19 crisis

The public finances, while still unbalanced, have been on a positive trajectory since 2022. The Covid crisis threw the public finances out of balance, with the budget deficit rising to 6.5% of GDP in 2021. Since then, the government has been working to gradually reduce the deficit, notably as part of the new public finance plan (Public Finance and Fiscal Responsibility Act) passed in 2023, aligning Malaysia’s budgetary targets with the Maastricht criteria (public debt of 60% of GDP and a budget deficit of less than 3%). These efforts appear to have borne fruit: the budget deficit fell from 5.1% of GDP in 2023 to 3.7% in 2025, an improvement that exceeded official forecasts. The target of 3% by 2028 thus looks achievable.

These efforts have mainly involved streamlining subsidy programmes and diversifying revenue sources. The largest household subsidies (for fuel and some food products) have gradually been recalibrated to reduce the beneficiary base. At the same time, new revenue sources have been created: the sales and services tax, introduced in June 2025 to replace the goods and services tax, offers slightly better revenue prospects. The 2026 budget assumes a 2.7% increase in revenue, a 1.8% increase in current expenditure and a 1% increase in investment and development expenditure.

Government revenue still too reliant on oil

Malaysia still has too few sources of tax and non-tax revenue outside of oil. Informal work still accounts for a significant share of labour, reducing the tax base, despite the introduction of measures like electronic invoicing. The tax burden is the lowest in the ASEAN region (12.6% in 2024). Dividends paid by state-owned oil company Petronas still account for a significant proportion of non-tax revenue (20% in 2025), exposing the public finances to oil price volatility.

Public debt: high but on the right track

Public debt remains under control and the public debt to GDP ratio is set to decline by 2030. The public debt ratio has stabilised at around 70% and should begin to gradually come down from 2030 onwards if the public finances remain on the same trajectory. Ninety-eight percent of the debt is denominated in local currency and 80% is held by resident investors. Refinancing is almost entirely reliant on domestic capital markets. In recent years, the government has worked to extend the average maturity of debt through long-term issues. The weighted average interest rate on government borrowing is 3.8%, reflecting investor appetite.

Malaysia is also keen to position itself as a global leader in Islamic finance and uses a wide range of instruments to achieve this goal, starting with public debt: 8.9% of borrowing in 2025 was through Malaysian Islamic Treasury Bills and Shariah-compliant securities, highlighting the country’s desire to leverage Islamic finance for refinancing purposes. Such instruments are regularly included in central government refinancing programmes, encouraging the expansion of the sector through the large-scale issuance of low-risk securities. In its 2024 activity report, Banka Negara Malaysia (BNM, the Malaysian central bank) pointed out that the market share of Islamic finance was as high as 46.6%.

A weakness to watch: external debt

While external debt has not reached worrying levels, it still exposes the country to refinancing risks in foreign markets. The external debt to GDP ratio stood at 69.6% at the end of Q3 2025; 57.5% of the debt is of medium-to-long-term maturity and two-thirds is dollar-denominated. The majority of short-term debt is borne by the private sector, making it vulnerable to shifts in capital flows and/or interest rate movements. Debt holdings remain relatively diversified, but the external financing requirement stands at 28% of GDP, well above the recommended threshold of 15%. The risk remains manageable: the country has a good level of foreign exchange reserves ($111 billion excluding gold, equivalent to 4.7 months’ worth of imports) in addition to the sovereign wealth fund’s $15 billion-worth of dollar assets. The external financing requirement is expected to gradually ease, falling to 25% of GDP by 2028.

Internal obstacles to achieving the government’s growth targets

An increasingly fragile coalition government

Prime Minister Ibrahim Anwar’s coalition government is looking increasingly fragile. The prime minister’s party, PH, performed particularly poorly in the last federal elections, losing eight of the nine seats it formerly held in the state of Sabah. Two major government-sponsored bills (one of them to introduce term limits for prime ministers) were recently rejected by the House of Representatives.

2026-2027 will be a pivotal period for the country’s political stability. Three federal elections are scheduled to take place during this period and could profoundly alter the delicate parliamentary balance. A general election must be held sometime before December 2027. However, depending on the political dynamics, a tactical dissolution (a common tradition in Malaysia) is a possibility and could come before the end of 2026, which would align with some local elections (thus keeping costs down). The end of the year is also often a more buoyant period economically speaking.

A tense sociopolitical climate

The sociopolitical climate encourages ethno-religious tensions. The main Malay nationalist party (UMNO), part of the government coalition, recently said it wanted to form a coalition of parties championing Malay interests for the next general election. Prime Minister Anwar is effectively locked into policies that favour the Malay population at the expense of other minorities (populations of Chinese and Indian origin, etc.), which had previously given him their strong support. Such policies are part of a long tradition of electoralism and clientelism. Forthcoming elections are likely to heighten this climate of confrontation.

The highest levels of government remain rife with corruption. Prime Minister Anwar, himself previously convicted on multiple charges, is frequently suspected of wielding corruption accusations as a way of silencing the opposition. One of his political rivals, former Prime Minister Najib Razak, had already lost power largely because of corruption allegations against him and his entourage. A royal pardon could pave the way for him to make a political comeback. The Malaysian Anti-Corruption Commission still enjoys relative popular support, since it is going after members of both the government and the opposition.

External risk factors: uncertainty at the heart of international trade and the closure of the Strait of Hormuz

International trade, one of the country’s strengths, remains a source of uncertainty for 2026

The country’s flagship exports continue to perform well, benefiting from a positive trend. As well as natural resources, Malaysia mainly exports electronic equipment and spares. It once again ran a large trade surplus in 2025.

However, Malaysia is reliant on both exports to the US and imports from China. Exports to the US account for 23% of total exports – a risk factor in an uncertain trade environment. However, they appear to have withstood the Trump administration’s tariffs: Malaysia’s trade surplus with the US fell only slightly in 2025. At the same time, 36% of its imports are from China, making its role as a trade hub somewhat precarious in the context of a trade war.

The recent US Supreme Court ruling overturning most of the Trump administration’s import tariffs encouraged Malaysia to declare its trade deal with the US null and void, positioning it as the first country to make such a decision. There is currently little long-to-medium-term visibility on the next framework agreement with the US on potential trade tariffs.

Hormuz: limited impact but worth watching

Malaysia is known as a hub for Iranian crude oil: nearly 80% of Iranian oil destined for China is thought to pass through Malaysia, where it is transhipped and categorised as Malaysian oil, thus boosting the country’s export numbers. Although the conflict has brought these flows to a halt, Malaysia’s energy supply is not fundamentally at risk. As a producer of both gas and crude oil, the country is less exposed than its neighbours.

Malaysia also has substantial coal reserves, which means it could continue to generate electricity in the event of a shortage of gas (its main source of power generation). Higher energy prices (oil and LNG) should boost government revenue, though this will be offset by higher spending on fuel subsidies, with fuel prices likely to rise. Relatively speaking, the country should thus emerge as a beneficiary of the conflict compared with some other harder-hit countries in the region (India, South Korea, the Philippines, etc.).

Inflationary pressures should thus remain contained, though Malaysia is also exposed to transmission channels other than energy prices. Tourism accounts for nearly 15% of Malaysian GDP; while airlines say it will take at least a few months for the situation to return to normal, the absence of Europeans (around 15% of tourists, but with high purchasing power) could affect foreign exchange inflows, employment and consumption.

Malaysia has pulled off a spectacular fiscal recovery and now benefits from a privileged position at the heart of international trade, strong demand driven by artificial intelligence – boosting its exports – and a highly favourable growth outlook. Despite external risks to the economic environment – uncertainty over the resumption of trade in the Hormuz region, value chain disruption – the biggest threat to the country’s trajectory may be domestic.

If the outcome of the next federal or general election were to erode political stability or cause the government coalition to implode, the country could be plunged back into political instability of the kind that was so damaging during the Covid-19 crisis. Amid heightened ethnic and religious tensions, this scenario should be avoided at all costs if Malaysia wants to stay on course to become the high-income economy it aspires to be.

[1] The Gini coefficient is a measure of income inequality among the population ranging from zero (less unequal) to 1 (more unequal).